June

16, 2021

8 min read

This story originally appeared on StockNews

2021 has been brutal for growth stocks as many names are down between 25 and 40%. However, a handful is bouncing back. Taylor Dart identifies two more stocks that investors should look to buy on weakness: Snap (SNAP) and Zoom (ZM).

It’s been a volatile year thus far for the Nasdaq Composite (COMPQ), with the index up 9% year-to-date but enduring two sharp corrections along the way. Typically, this period of consolidation would have unearthed many values plays in the tech space, with valuations having time to play catch-up through this period of digestion. However, with more than 30 names still trading at more than 40x sales, and the price to sales ratio for the S&P-500 (SPY) in nose bleed territory at record levels, it’s much harder to find the value out there lately. This isn’t surprising after a 113% rally for the index in barely 15 months. Fortunately, two names have held up well over the past couple of months and looking to be showing strength relative to their peers. These two names trade at reasonable valuations and could be two solid buy-the-dip candidates if we do see a shake-out in the market.

(Source: TC2000.com)

Zoom Video (ZM) and Snap Inc. (SNAP) both had incredible years last year and broke out of large IPO bases, but both have spent the past several months correcting, which has brought them both to much more reasonable valuations. While Zoom Video is a Computer-Software name and was the leader of the stay-at-home trade, Snap comes from the Internet-Content industry group and has seen tremendous progress the past year in its key operating metrics. Both companies boast market-leading revenue growth rates of 60% or higher. While Zoom already has earnings on the table, Snap is set to post its first year of positive annual earnings per share in FY2021 if it can continue to see an acceleration in its business. Low-growth value plays have recently been the most in vogue, but it might be time to start looking at the high-growth value plays, and Zoom and Snap Inc. both look like solid bets if we see continued weakness. Let’s take a closer look below:

Beginning with Zoom, it’s no secret that sentiment is poor on the stock, with the stock falling more than 50% from its highs as investors brace for lower demand due to the re-opening trade. However, while some investors believe that growth will come to a grinding halt, the company’s numbers show something different, with revenue set to come in above $4.1BB in FY2022, up from $2.65BB in FY2021. This is the furthest thing from a slowdown, with a projected 55% revenue growth rate this year. This incredible growth is because while many businesses will not be using Zoom as much, schools (given Zoom for free) will have to start paying, and many are likely to renew their contracts.

Elsewhere, we haven’t seen any serious churn thus far in fiscal Q1 2022, with the company’s net dollar expansion rate remaining above 130% for the twelfth consecutive quarter. So, while some churn is likely, the good news is that new products (Zoom Phone Appliance), and major wins with large companies that prefer the convenience should more than offset the lost contracts with other users that are anxious to return to normal without the use of Zoom Video for business operations.

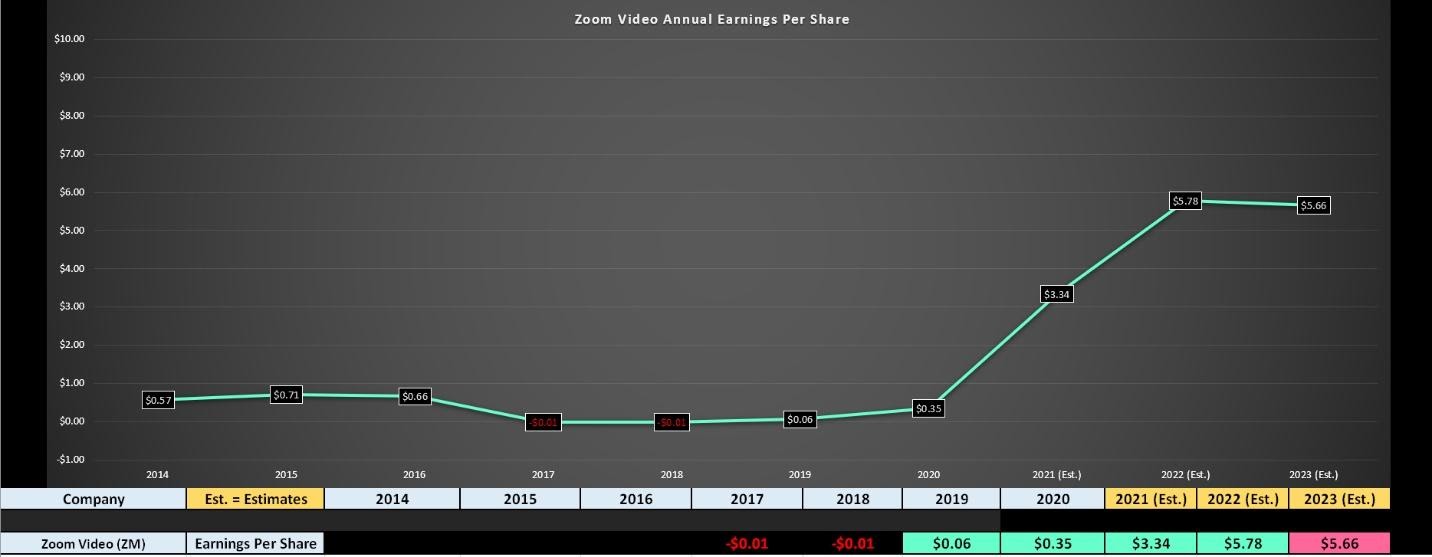

(Source: YCharts.com, Author’s Chart)

It might be crazy to think of Zoom as a value play with $3.34 in annual EPS in FY2020 and a share price above $350.00. However, if we look at FY2022 estimates, annual EPS is expected to increase to $5.78, nearly doubling after a year of more than 900% growth. These types of growth metrics are unheard of, making Zoom one of the highest growth names in the market currently and easily capable of commanding an earnings multiple above 100. The caveat is that FY2023 annual EPS estimates are expected to drop off as the economy returns to normal, but I think it is mostly analysts leaning to the conservative side. If Zoom’s new products can gain traction and large Fortune-500 wins continue, there’s no reason that annual EPS can’t increase in FY2023 as well.

If we use a more conservative earnings multiple of 75 for Zoom and FY2022 annual EPS estimates of $5.78, Zoom looks quite cheap, with a fair value closer to $433.50, or nearly 25% above current levels. This assumes that the company doesn’t beat on annual EPS and has guided aggressively with $4BB in revenue, which I don’t think is the case. Given the unprecedented landscape for Zoom and potential headwinds, I wouldn’t be surprised if the company sand-bagged guidance and is set to deliver a massive beat. So, while 25% upside might not seem significant, this assumes no beat on earnings which looks like a high likelihood.

Notably, the stock has changed its character, recently breaking out of its downtrend and showing some accumulation the past few weeks. This accumulation doesn’t preclude a pullback, but it does suggest that any pullbacks below $340.00 will likely provide low-risk buying opportunities. In summary, if we see weakness in ZM, I would view this as a low-risk area to start a position in this high-octane growth name.

(Source: TC2000.com)

Moving over to Snap, the company also came off a great quarter with revenue of $796.9MM, up 66% year-over-year. Amazingly, this was an acceleration from the 62% growth rate it posted in Q4 2020 ($911.3MM in revenue), and this was the highest growth quarter in the past two years. On a two-year stacked basis, Snap’s revenue growth rate dwarfs most of its peers in the Internet-Content group with a 110% two-year stacked revenue growth rate. These incredible results were driven by continued growth in daily active users [DAUs] to 280MM, up from 229MM in the year-ago period. Notably, growth in the rest of the world is accelerating the most, up from 71MM to 111MM, while the company continues to add to its DAUs domestically despite incredible growth already.

Currently, SNAP estimates that it has a 23% penetration of North American smartphones and just a 5% penetration in the rest of the world, where it has just 111MM DAUs. This suggests that the story is still very early for Europe and the rest of the world, where the company believes its penetration rate is in the single digits (14% Europe, 5% Rest of the World). Most importantly, while DAUs have been increasing rapidly, average revenue per user has also soared, up over 20% in FY2020 to $10.09. In the same period, infrastructure costs per DAU have fallen 5% to $2.78.

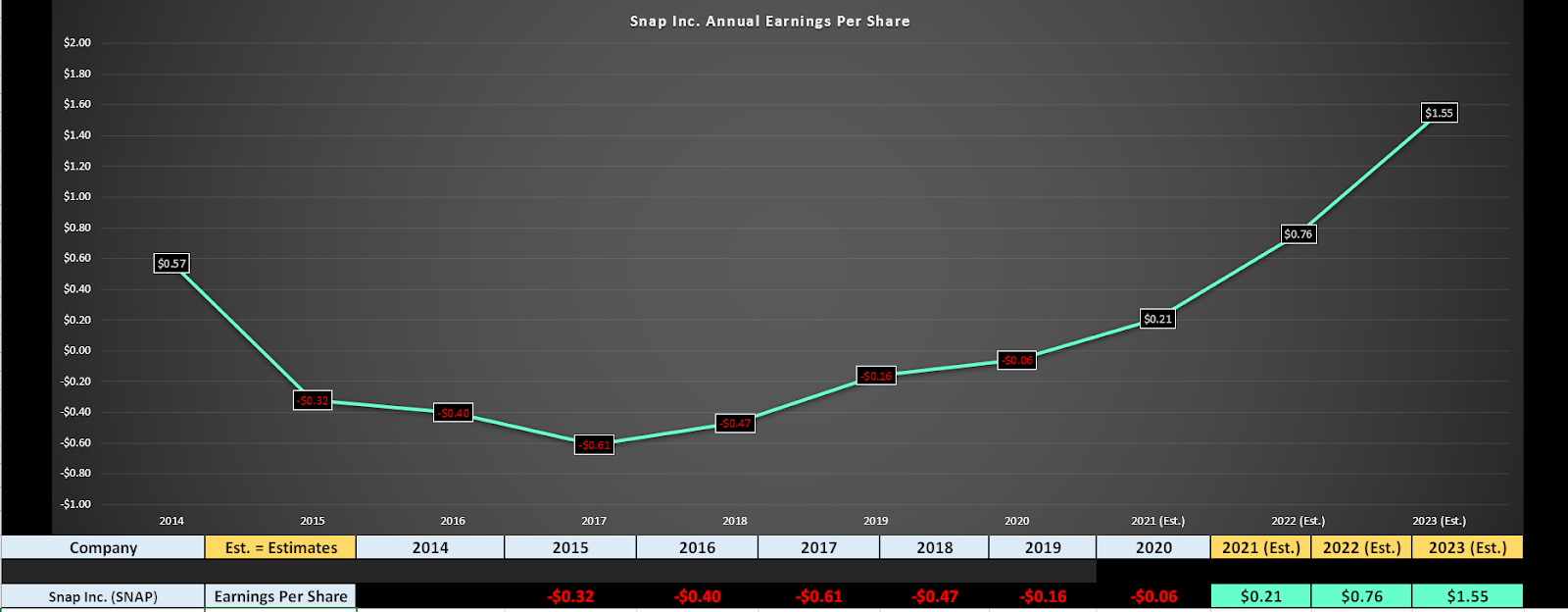

(Source: YCharts.com, Author’s Chart)

If we look at the chart above, SNAP is set to see a material improvement in its earnings trend, with FY2021 annual EPS set to turn positive and FY2022 annual EPS set to increase by more than 300% year-over-year. These are lofty estimates relative to the consensus currently. Still, I believe they’re achievable if the business continues to accelerate this year, which seems likely with more interaction and reasons to ‘snap’ as we see a re-opening of economies globally. Based on what I believe to be a fair earnings multiple of 60 given the growth rates here, SNAP looks very reasonably valued relative to its FY2023 annual EPS estimates, with a fair value of $93.00. This translates to more than 45% upside from current levels. So, if the stock does pull back below $55.00, where it would have more than 50% upside to its fair value, I would view this as a buying opportunity.

As shown below, this is the first base for the stock since breaking out of a massive IPO base, and the odds suggest that the stock will break out to the upside and move higher after digesting its gains for several months. Of course, there are no guarantees, but buying in the lower end of this base closer to $55.00 looks like a decent reward/risk bet.

(Source: TC2000.com)

While it’s tough to find the value out there in the tech space, SNAP and ZM look like two solid bets if we do see market weakness over the coming months. In summary, I would view sharp pullbacks to the levels noted above as low-risk areas to start positions.

Disclosure: I am long ZM

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

SNAP shares were trading at $62.39 per share on Wednesday morning, up to $0.11 (+0.18%). Year-to-date, SNAP has gained 24.61%, versus a 13.98% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 2 Tech Stocks To Buy On Dips appeared first on StockNews.com