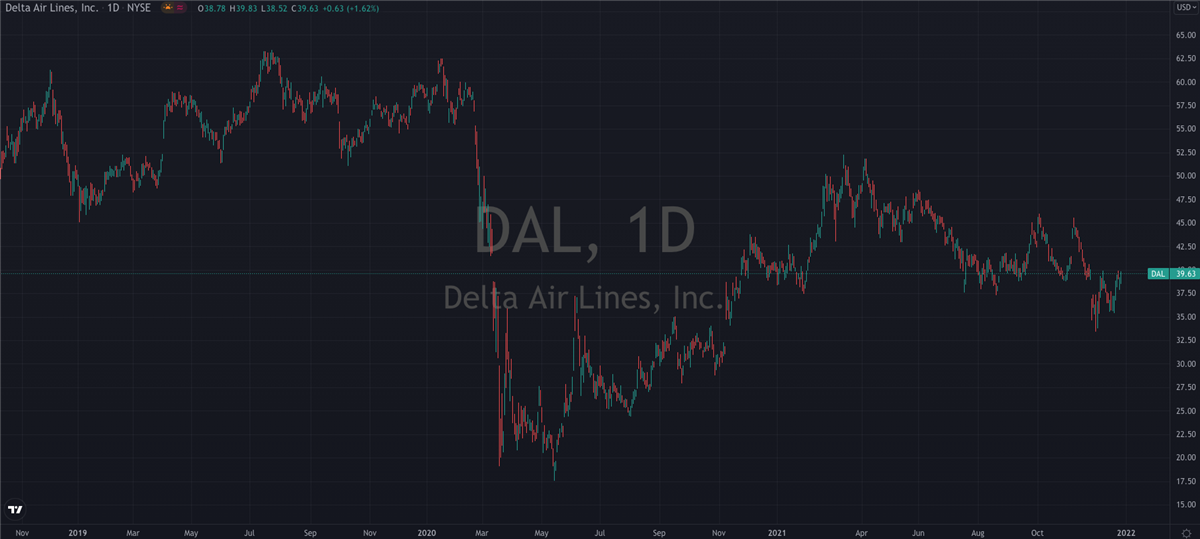

With consistent higher lows being set on their stock’s chart for much of the past year, there’s a lot to like about Delta Airlines (NYSE: DAL) right now.

Free Book Preview

Money-Smart Solopreneur

This book gives you the essential guide for easy-to-follow tips and strategies to create more financial success.

June

10, 2021

4 min read

This story originally appeared on MarketBeat

With consistent higher lows being set on their stock’s chart for much of the past year, there’s a lot to like about Delta Airlines (NYSE: DAL) right now. The $30 billion airline major has been riding the reopening wave that’s raised it and its peers a long way above the dark days of 2020. The 170% shares have tacked on since the lows of last year are testament to that.

But even with the vaccine rollout and full economic reopening continuing to near completion, that doesn’t mean the edge is gone. If anything, there are plenty of signs suggesting the best is yet to come. Earlier this week, the folks over at Jeffries boosted their rating on the stock from Hold to a Buy, and called them the best positioned of the majors for the next stage of the recovery. With TSA traffic back to 70% of its 2019 levels, that’s a bullish statement to be making.

Fresh Upgrade

Analyst Sheila Kahyaoglu summed up the team’s view when she said “about half of Delta’s sales are corporate, and we think its 50% exposure to SMB travel should drive some share gain as corporate travel restarts. In addition, Delta has outsized transatlantic exposure versus its peers. We see 30% potential upside to 2023 earnings power, driven by yield improvement, lower expenses and lower fuel costs.”

They’re also forecasting 2023 EPS to hit $7.60, a current street high, and a print that would confirm a remarkable turnaround from the non-GAAP EPS of -$3.55 which Delta posted in April’s Q1 report. This would be slightly higher than their pre-pandemic expectations for 2020’s EPS and if you’re inclined to buy into Jefferies’ bullishness, then herein lies the opportunity. Delta’s stock is still trading 25% lower than its pre-COVID levels, a gap which it should easily eat into and fill over the coming months if the recovery trend maintains its trajectory.

At their presentation at the Bernstein Strategic Decisions Conference last week, CEO Ed Bastian made it clear the company expects this of themselves and gave some indications that their recovery strategy is paying dividends already. He increased guidance for Delta’s Q2 revenue and thinks their pre-tax loss for the quarter will be better than expected. By the end of this month, Bastian is also expecting domestic leisure travel to be 100% restored, with their cost per available seat mile getting back to 2019 levels by the end of the year.

Strong Trends

An impressive statistic from this year’s Memorial Weekend shows why this goal should be easily achievable. Domestic leisure tickets sales were up 30% compared to the same holiday weekend in 2019. Tickets booked through corporate channels are showing consistent improvement also and were down -58% compared to 2019 versus -67% the previous week. This is all the more impressive considering key corporate cities like New York and San Francisco weren’t even fully reopened in May. This growing recovery potential has been picked up on by CFRA too, who called Delta a key recovery name in their latest list of stocks with ongoing positive exposure to the global vaccine rollout.

The passenger traffic rebound is still gathering pace and Delta has undoubtedly made the most of it so far. Technically, shares have been consolidating in a narrowing range since February and look poised for a breakout in the coming weeks. For those of us on the sidelines and considering adding some airline exposure to our portfolio, Delta has to be considered one of the stronger picks out there.

Pick Of The Bunch

Towards the end of last month Morgan Stanley said they came away very impressed from meetings with Delta’s executive team. They went so far as to say that Delta is the only legacy airline they’re covering that has an Overweight rating at Morgan Stanley. The company’s strong franchise base, customer loyalty and historical margin superiority are expected to continue on the other side of the pandemic.

With shares still trading at a significant discount to their pre-pandemic levels, it’s not unreasonable to think that in the not too distant future we’ll be scratching our heads about how they stayed down here for this long at all.

Featured Article: What is Cost of Goods Sold (COGS)?