February 5, 2021 7 min read

Opinions expressed by Entrepreneur contributors are their own.

Recently it was reported that a deputy from Morena is proposing to reduce the time of permanence of delinquent clients in the credit information companies or SIC (such as Buró de Crédito (BC) and Círculo de Crédito (CC)) as a measure to “reactivate the economy” . The proposal proposes reducing said permanence from 72 months to 18 months, and the justification lies in the difficulties that customers have to pay, a situation enhanced by the pandemic we are experiencing.

I consider this to be a mistake, by reversing the ground gained in the emphasis and importance that people should have with their personal finances and their credit history; by punishing those who have paid correctly for the lack of information, depriving them of possible better rates and credit conditions; and by damaging innovations in the granting of credit faster, with better conditions and at a distance, whose only input is the need for information.

I believe that the proposed Law is well intentioned, and that, appealing for the supposed interest of the people, it is presumed that it will improve the granting of credit. However, as the founder of Prestadero, the platform that, using information from the SICs, managed to be the first to grant loans 100% online in Mexico without endorsements or guarantees, the information gap that this proposal would generate would prevent us from granting loans with better conditions , harming the very people that this proposal seeks to help.

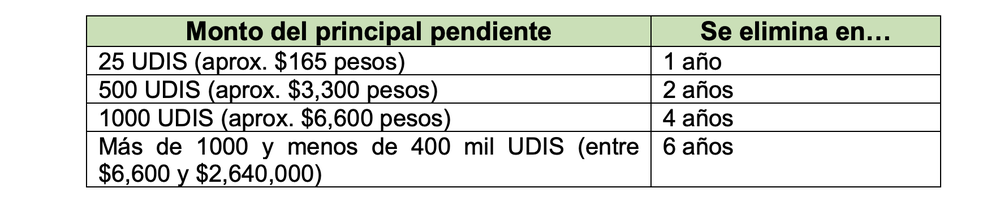

The current Law already stipulates through Banco de México rules in Circular 27/2008, that loans of low amounts will be eliminated from the credit history, including, in some cases, earlier than the proposed Law proposes.

This Law, then, tries to downplay the importance of debts of high amounts and could generate a perverse attitude, when requesting credits of amounts up to $ 2.64 million, stop paying, and wait only 18 months for the credit to be eliminated from your history with impunity (loans of larger amounts are not eliminated, and I would assume that the proposal does not consider the reduction of the permanence in loans greater than 400 thousand UDIS).

And what happens to those users that credit grantors reward for their good behavior, and who have not even stopped paying during this pandemic? We will punish them for that lack of information evenly, adjusting our rates up for this additional risk.

For example, suppose that two users apply for a loan in Prestadero: Ana and Pedro. Let’s suppose that Ana and Pedro have exactly the same credit history, but with one exception: Ana has a debt that she stopped paying 5 years ago. Therefore, Ana’s loan is approved at a rate of 20% per year and Pedro’s loan at a rate of 10% per year, based on her credit performance. Now suppose that the Law proposal to reduce the permanence of delinquent clients is approved, in such a way that the credit that Ana stopped paying 5 years ago is eliminated, so that the records of Ana and Pedro (who always paid on time) they are identical. Due to the knowledge that negative credits are already visible for much less time, Prestadero adjusts its risk model, granting Ana and Pedro the loan at 15% per year. Is it fair that Pedro now cannot access the same credit conditions as before when he always paid on time? Of course not. The proposed Law assumes that the grantors will not make changes to our risk models if it is approved, but that will not happen, and therefore, those most affected if this proposal is approved are the best payers.

It must be remembered that it is not the Credit Information Society that grants you the credit, and that a person is negatively reported or not in the Credit Bureau is not a sine que non requirement of obtaining it. For this reason, innovative companies are constantly emerging that seek alternative ways to perform credit scoring, and that take factors (such as the current pandemic) to determine if the person stopped paying due to force majeure and not due to lack of will (which can be inferred very easily).

Even Prestadero has a credit product called Prestapal in which you do not need to have a good credit history, and we help to reintegrate you with your good payment behavior to the financial system . But for these products to exist we need to have access to information. These types of innovations should be the basis for the country’s growth and reactivation of the economy, not the exclusion or elimination of information that disables this innovation.

Grantors, with a simple analysis of a person’s credit history, can identify if the credit or credits were defaulted during the evolution of the pandemic to determine the probable cause of the delays. The proposed Law could even ask the SICs to introduce a new observation code to the credits that were delayed during the pandemic, and thus the grantors could discern with even greater ease (and make the decision not to take into account), the delays due to COVID-19 . However, if eliminating the information completely does not give that option to the grantor, then the risk model will be modified to harm everyone to the letter.

Another of the potential negative side effects of this reform of the Law could be the substantial increase in judicial processes to recover the debt, since, in the event that the credit is in judicial process, it is not eliminated from your record (not even in sixdfgh years). Prestadero would surely carry out this strategy, filing massive lawsuits even with clients who are willing to pay, but with delinquent credits to avoid the elimination of the records in their history. When it comes to loans without collateral and without guarantees, the credit history is your best cover letter; But if that letter is not shown complete, and the penalty for stopping paying in your history is null or low, then it automatically detracts from the history of people who have always paid on time.

It should be noted that I have not had access to the proposed Law, and I have only identified its precepts through interviews and reports, so I reserve the right to modify or attenuate this point of view if the Law has details that contradict what I present here (For example, that the reduction of permanence is only on certain amounts and / or that it is only on loans due during the period of the pandemic).